Despite pulling back on linear television and theatrical production spending, the Walt Disney Company remain the world’s biggest investor in motion picture content, according to a new report released by Ampere Analysis this week.

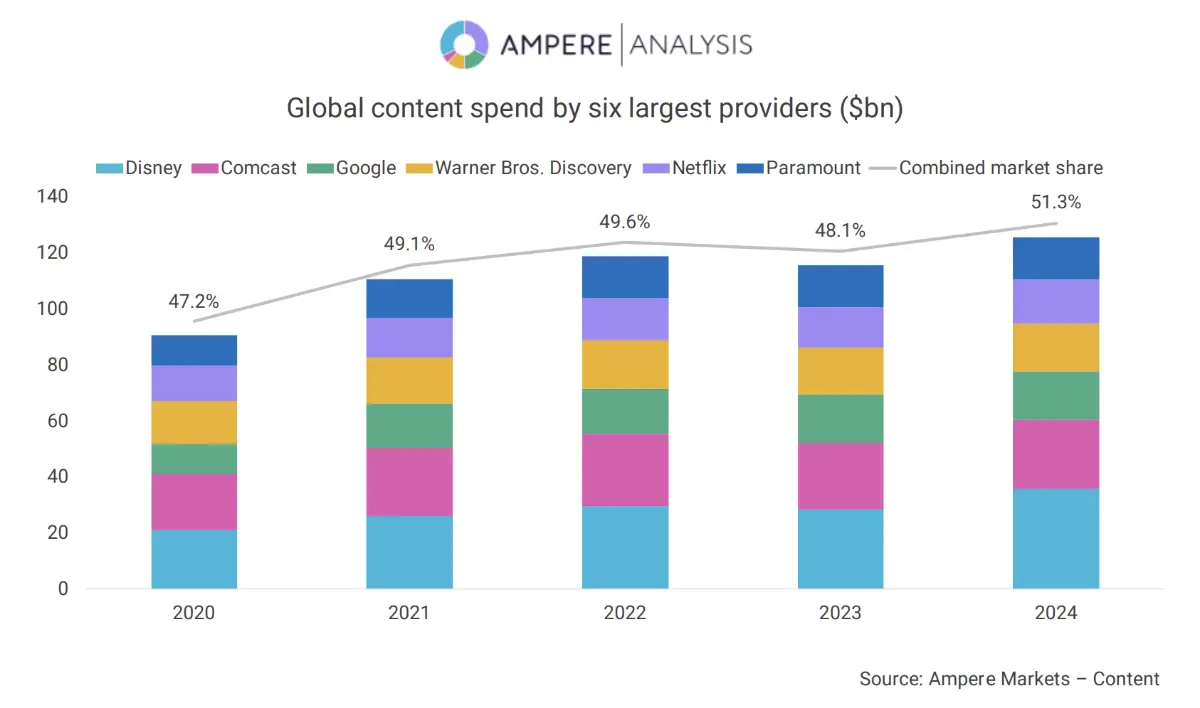

The report said the six largest media and entertainment brands are responsible for over half of the world’s content investments. The other five brands reflected in Ampere’s annual report include Google (YouTube), Netflix, Comcast (NBC Universal, Sky Group), Paramount Global and Warner Bros Discovery.

Disney accounted for more than 30 percent of all content spend, helping to boost its broadcast and cable networks in the United States (including Disney Channel, FX and ABC), as well as its global streaming platform Disney Plus. The company also operates ESPN Plus and Hulu in the United States, Star in overseas regions and a handful of linear pay TV networks in Europe, the Middle East and Latin America.

Google contributes to the world’s content investments by operating a revenue-sharing program that cuts creators who publish through its YouTube platform in on revenue generated from ads and sponsorships sold against those videos, Ampere said. It also splits revenue from the sale of YouTube Premium subscriptions when members stream content from YouTube partners; YouTube Premium allows viewers to stream most videos without Google-inserted advertising.

The other four media brands utilize a mixture of traditional television, theatrical film and streaming platforms to get their TV shows and films in front of audiences — except Netflix, which operates exclusively through its own online subscription video on-demand platform. Netflix remains the top producer of streaming-only content, Ampere noted, spending $14.5 billion to produce its own films and TV shows, and acquire the licensing rights to events like two National Football League (NFL) games that will stream exclusive through the platform in December and the worldwide rights to the WWE’s weekly TV programs.

All told, the six companies have spent over $56 billion on global content production since 2022, representing 45 percent of their total spending, Ampere said. Of that, around $40 billion is spent supporting streaming video platforms, including Netflix, Paramount Plus, Peacock, Sky Showtime, Max, YouTube Premium and Discovery Plus.

“Ongoing investment by major studios and streaming platforms into new programming will continue to be key to keeping audiences engaged and entertained,” Peter Ingram, a research manager at Ampere Analysis, said in a statement.

Ingram said the content landscape continues to be impacted by twin Hollywood strikes — one involving writers, the other actors — that ground TV and film production to a halt last year. The strikes disrupted traditional broadcast and cable networks, which were forced to get creative in filling out their prime-time and weekend programming schedules, and the effect is still being felt on theatrical film and streaming releases, which were significantly delayed.

“We can expect that the content landscape will see low level growth in 2024 as production schedules recover from disruptions caused by the pandemic and the writers’ and actors’ union strikes.” Ingram noted. “Looking forward however, while these top six providers will continue to account for the majority of spend, overall growth will plateau as companies look to refocus their output. This will include limiting commissioning volumes and prioritizing strategic investments and profitability to counter the current challenges of the media market.”